The Quiet Exit

When the Fund Math Starts Without You

The view from either side of the table.

There is a moment, somewhere after the closing dinners and the welcome calls, when the math starts to run.

Not your math. Theirs.

PE funds do not measure success one company at a time. They measure fund-level returns. If a fund has fifteen portfolio companies, the partners are not equally invested in each thesis. They are watching which ones are compounding, which ones are flat, which ones are pulling operating partner attention away from companies that could move the needle. At some point, often within the first year, they begin to sort. Conviction gets allocated. Attention gets allocated. Capital reserved for follow-on gets allocated. The fund is one portfolio, not fifteen separate bets, and the partners are running the math on which bets earn more of the fund's finite resources.

The operator almost never sees this happen. The operator is running the company. The math is being run in a different room.

What the operator does see is the room going cool. The lead investor who used to take the update call from a beach in Sardinia now prioritizes family time, or has handed the slot to another portfolio company. The check-ins get shorter. Texts go unanswered for a day, then two. The operating partner who used to drop by is suddenly booked out three weeks.

Those are not mysterious signals. They are the visible output of the math.

I have sat on both sides of the table. The room does not feel different right away. It feels less, before it feels different. Less attention. Less push. Less argument over the variance. By the time you can name what changed, the math has already been run. The conversation has already been had somewhere else, in a room you were not in.

This issue is about that math, and about the conversation that should be happening on both sides of the table before the silence sets in.

Part One: The Fund Is the Customer

PE's job is to make the fund work. That is the assignment from LPs and that is the discipline the partners are measured against. A fund with one winner that compounds at thirty percent net of fees can absorb several write-downs and still return the fund. A fund that babies a struggling position at the expense of redeploying operating partner time to the company that is actually compounding is a fund that misses its mark.

Most funds are structured to give themselves room to make this call. The vehicle is often a secured note, sometimes convertible on milestones, sometimes converting on the fund's election if the thesis is proving out. Equity follows when the company is earning conviction. When it is not, the structure gives the fund a look-see period. They get time with the capital deployed to decide whether to convert, take control, or unwind the position to recover what they can.

That structure is rational from the fund's side. It also means the operator is running against an answer that has not been given yet. PE is still deciding. The operator is already executing as if the answer is yes.

Taking control is expensive. Foreclosure proceedings, parceling out assets, managing a CEO transition, defending against the counter-claims that often follow, all of it costs operating partner time and legal spend. For a fund with multiple positions to manage, the math frequently says write it down and redeploy. The write-down is not laziness. It is fund-level discipline. The capital is gone either way. The only remaining question is whether to spend more time and attention trying to recover some of it.

From the operator's chair, none of this looks like math. It looks like the lead partner stopped calling.

“PE is still deciding. The operator is already executing as if the answer is yes.”

Fifteen positions, finite attention, one fund.

Part Two: The Visible Math

The three stages of distancing are not random. They are PE's sorting process becoming visible, one signal at a time.

Stage one is enthusiasm. PE has not yet run the fund math on you. The deal is fresh, the thesis is alive, and conviction is still tied to underwriting. The lead investor takes the update call from a vacation rental in Sardinia because they have not yet measured you against the rest of the portfolio. Intros come unsolicited. Resources show up before you ask. For a moment you are the most important company in their portfolio, because for a moment you are.

Stage two is professionalization. The math has started. The cadence becomes formal. Weekly calls move to biweekly, then monthly. Spontaneous contact disappears. Conversations that used to happen on a walk now happen in a board deck. The vacation call gets rescheduled, then rescheduled again, then handed to the associate with a polite note. Nothing is wrong. Everything has just become more efficient. Efficiency in an investor relationship is often the first sign that conviction is being reallocated to a different position in the fund.

Stage three is the math finished. Legal gets looped in on questions that used to be operational. Expenses get scrutinized at a level of detail no one cared about six months ago. Cash runway becomes the only topic. The operating partner who used to drop by is now booked three weeks out. You are no longer being managed toward upside. You are being managed toward an outcome the fund has already chosen.

Most operators only recognize stage three. By then, the math has been run, the answer has been given, and the only remaining question is which exit path costs the fund the least. The work of operational literacy is to read stage two, while the math is still being run and the answer has not yet been recorded.

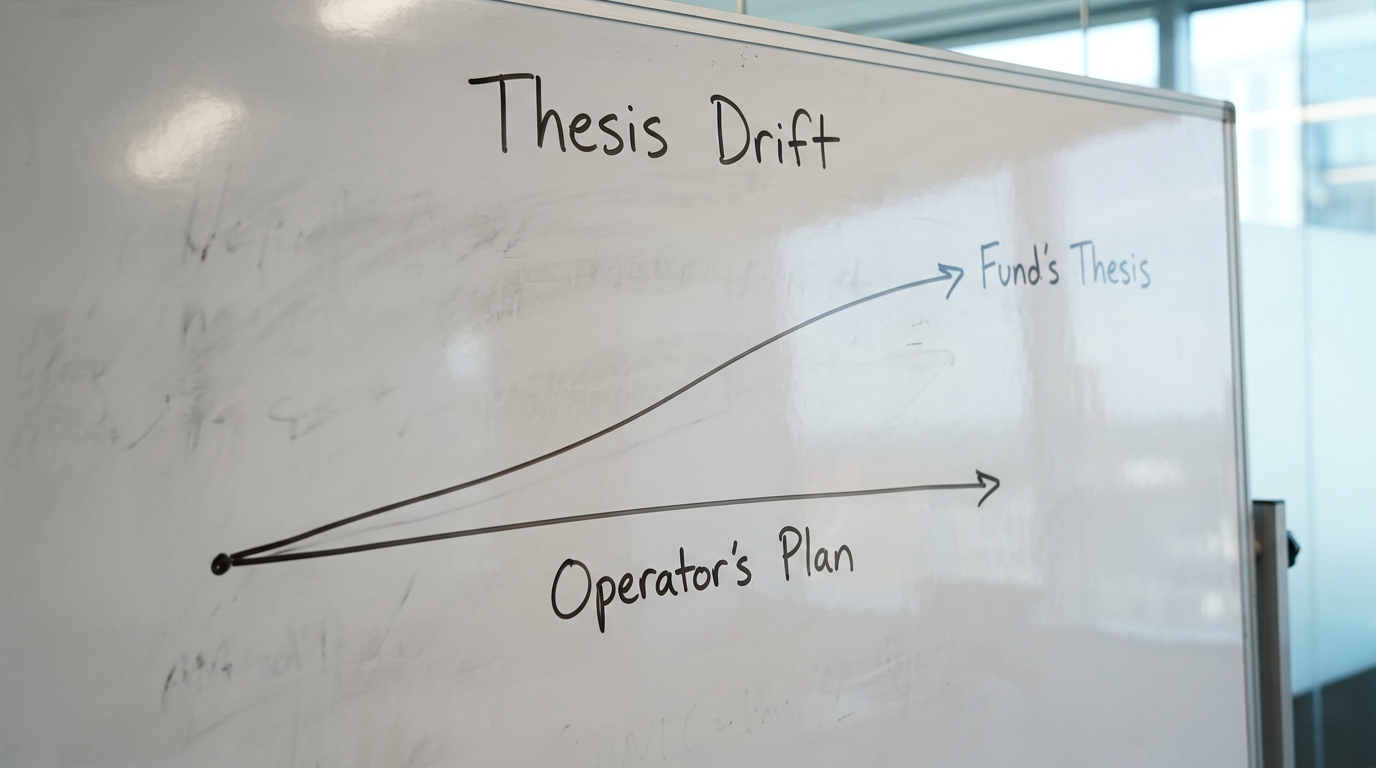

Part Three: The Thesis Drifts on One Side of the Table

At close, PE and the operator agree on what winning looks like. The thesis is shared. For the first months, everyone is running the same play.

Then the PE team starts to see something the operator has not yet named. Maybe it is a competitive move that rewrites the assumptions. Maybe it is a margin path that looks different than what was modeled. Maybe it is a comp set that is compounding faster, which makes the original thesis look slower by comparison. The deal team watches the data. They have conversations internally. They adjust their conviction on what the company needs to do, or whether the company is still the right place for the fund's attention.

And then they do not circle back to the operator and say: "Our thinking has evolved. Here is what we are seeing. Here is how that changes what we need from you, or whether we still believe the original plan is the right one."

Instead, the thesis drifts. The operator is still executing against the plan from close. The PE team is now measuring against a thesis that has evolved internally, often in comparison to other portfolio companies that are proving their theses faster. The variance between the two grows quietly. It is invisible at first. Then it is not. The operator misses a forecast the PE team was no longer expecting them to hit. The board meeting gets tighter. The questions change. The operator feels the room cool without understanding why.

The room cooled because the thesis changed without them.

This is not a story about PE being deceptive at close. It is a story about operational discipline failing in the middle. PE saw something, made a judgment, evolved their thesis internally, and did not make that evolution a conversation with the operator who is still running the company against the original plan.

“The room cooled because the thesis changed without them”

What evolves on one side of the table.

Part Four: The Operator's Question

The most useful thing an operator can do, the moment they feel the room begin to cool in stage two, is stop trying to read the signals and ask the question directly.

Not "how are we tracking," which gets a polite answer. Not "is everything okay," which gets reassurance. The question is sharper than that.

"Has your thesis on this company evolved since close? If it has, I need to understand how, because I am still running the original plan and I want to make sure we are aligned on what winning looks like from here."

That question does something the polite ones do not. It forces PE to either confirm the original thesis is intact, in which case the engagement should return, or to acknowledge that their thinking has moved, in which case the realignment conversation has finally started. Either answer is useful. Continued silence after that question is itself an answer.

The harder version of the same question, the one to ask when stage two is well underway and the signals are getting louder: "Where does this company sit in the fund's conviction stack right now? Are we still a position you are building, or have you started measuring us against a write-down decision?"

That is an uncomfortable question for a PE partner to answer directly. It is also the question that ends the ambiguity. Operators who can ask it have agency. Operators who wait for PE to volunteer the answer end up burning months against a thesis the fund has already mentally abandoned.

The temperature is not the data. The economic incentive behind the temperature is the data. PE is optimizing for the fund. The operator's job is to surface that conversation while there is still room to do something with the answer.

Part Five: What PE Owes the Operator

Operational discipline in PE is not just deal selection and value creation. It is also the discipline of the difficult conversation.

When the thesis evolves, PE owes the operator a realignment conversation. Not a board deck, not a memo, a conversation. "Here is what we are seeing. Here is how our conviction has shifted. Here is what we need from you to keep this position in the active build column rather than the triage column." That conversation is uncomfortable on both sides. It is also the conversation that prevents months of misaligned execution and salvages what can still be salvaged.

When the math has been run and the answer is leaning toward write-down, PE owes the operator the clarity of saying so. Not in those words, necessarily, but in a form the operator can act on. "We are no longer prepared to follow on. We need to find a path out of this position together." That clarity is hard for a PE partner to deliver because it ends the optionality the secured note structure was designed to preserve. It is also the most respectful thing they can do for an operator who is otherwise burning their own credibility and capital against a foregone conclusion.

The operator should understand what that clarity actually means. The shift from working together as a team to sitting on opposite sides of the table to negotiate an exit can feel like betrayal. It is not. It is the moment the relationship changes from build to wind-down, and both sides have to operate accordingly. Recognizing that early, rather than carrying the build posture into a negotiation that has already begun, is how operators protect their own position and reputation through the transition.

When the move is to take control, parachute in a new CEO, or pursue litigation, PE owes itself an honest answer to one question first. Is this a leadership problem, or is this a thesis problem? Because if the original thesis was sound and execution failed, a leadership change can work. If the thesis itself was the issue and got quietly abandoned mid-stream, a new operator running against the same model will not prove it either. They will burn more capital, more legal spend, more operating partner attention, and arrive at the same write-down the original team would have. Leadership executes a thesis. It does not invent one after the fact.

Funds that go further in to try to save an investment are not making a mistake by trying. They are honoring the capital their LPs entrusted to them. The mistake, when it is made, is in mistaking new leadership for a new thesis, or in avoiding the conversation that would have surfaced the misalignment while the original team could still have acted on it.

“Leadership executes a thesis. It does not invent one after the fact.”

The conversation that should happen.

The Takeaway: The Conversation Underneath

Issue 04 said it plainly. If you took PE money, you are for sale. Issue 05 is the harder corollary. The fund, not the company, is the customer. When the fund math starts to run against you, the silence follows, and the exit comes in whatever form is cleanest for the portfolio.

That math is not personal. It is not a verdict on the operator. It is the partners doing their job for their LPs. Understanding that is the difference between reading the silence as rejection and reading it as data.

The work, for both sides, is to make the difficult conversation a habit before the silence makes it impossible.

For the operator, that means asking the questions that do not get polite answers. "Has your thesis evolved? Where do we sit in the fund's conviction stack right now?" The answers, or the silence that follows them, are more useful than another quarter of professional cadence.

For the PE partner, the responsibility runs further upstream. It begins at close, with the discipline to make the thesis a shared agreement rather than a delivered plan. It continues with the willingness to take the call from Sardinia when the variance is real, especially then. It requires the discipline to realign openly when the thesis drifts, and the honesty to name a thesis problem as a thesis problem rather than reframe it as a leadership problem after the room has already cooled.

Funds owe a discipline to their LPs. Operators owe a discipline to the cap table. Both owe the discipline of the conversation to each other. The silence is not an act of nature. Someone chose not to make the call.

By the time the room is cold, the math has already been run. The TGVR mission is to surface the conversation while the room is still warm enough for it to matter.

Luciano Global Ventures Inc. | Interim and Transitional Executive Leadership | lucianogv.com

This article appears in TGVR Issue No. 05, June 2026, The Global Ventures Review, published monthly by Luciano Global Ventures Inc.